Yesterday we

posted the introduction to the chapter in which Dr. Harold G. Moulton

demolished the Keynesian money multiplier, which ironically, despite the fact

that it is based on an easily disproved fallacy, forms the basis of the

monetary and fiscal policy of virtually every government on Earth.

|

| Medieval (Deposit) Banking |

Understanding

Moulton’s explanation relies on understanding the nature of money itself, as

well as the function of the three different types of banks. We have gone over money many times on this

blog, so we need to focus on what a bank is and does.

As we said, there

are three basic types of banks, each filling a particular social and financial

need. Very briefly, these are:

I. Banks of Deposit. This is what most people think of as a

“bank.” A bank of deposit is defined as

a financial institution that takes deposits and makes loans out of those

deposits and its capitalization. A bank

of deposit does not create money.

II. Banks of Issue/Circulation. For all practical purposes, banks of issue

and banks of circulation are the same thing.

They are defined as financial institutions that take deposits, make

loans, and issue promissory notes that circulate as “current money,” i.e., “currency.” A bank of issue/circulation does not,

strictly speaking, create money, either, but functions to change one form of

money into another form of money more easily used to carry out financial

transactions.

III. Banks of Discount. A bank of discount is the only type of bank

that actually creates money. It does

this by accepting bills of exchange/commercial paper at a discount from the

face value, and issuing a promissory note to “buy” the bill or paper. This promissory note is negotiable, and could

be used as currency . . . except the denomination is usually far too large to

be useful for daily circulation, e.g.,

you cannot buy lunch with a $100,000 promissory note (traditionally the minimum

denomination for commercial paper), even though it is money the same as the one

cent piece in your pocket.

|

| Medieval Merchant/Mercantile/Commercial Banking |

Now, this is

where a little confusion creeps in. A modern

commercial, merchant, or mercantile bank (different names for the same thing) is a combination of all three types of bank. It takes deposits and makes loans out of

those deposits, thus acting as a bank of deposit. It also changes one form of money — accepted

bills of exchange and commercial paper — into a form more convenient for

transacting business, almost always these days by issuing a promissory note

used to back a new demand deposit. It

also accepts the bills of exchange and commercial paper, "buying" (accepting) them by issuing a promissory note that it uses to back

new demand deposits.

Paradoxically,

although many people think that commercial banks create money out of thin air

by creating demand deposits, it is easily seen that when a commercial bank

accepts a bill of exchange or commercial paper that it is really creating

asset-backed money. In contrast, when

the government emits “bills of credit” and the central bank “buys’ the bills of

credit (misleadingly usually called government bonds these days) by creating a

demand deposit or printing currency for the government, it really is creating

money out of thin air — or (more accurately) future taxes that might never be

collected.

So today we begin

looking at —

HOW THE COMMERCIAL BANKING SYSTEM MANUFACTURES CREDIT

|

| Harold G. Moulton |

It is the operation of the commercial banking system,

taken as a whole, that results in the creation of credit currency and thereby

adds to the total volume of circulating media. In order to make the process of

credit creation clear, however, it will be necessary first to analyze the

operations of an individual commercial bank. For this purpose we shall assume a

self‑contained community, that is, one having no financial relations outside

its own borders and having as yet no commercial banking institutions. Such an

assumption is not unrealistic, for it was under such conditions that the actual

development of banking began. We shall then broaden the analysis, in successive

steps, to include the several banks which may exist within a given community,

and, finally, all of the banks within a nation as a whole.

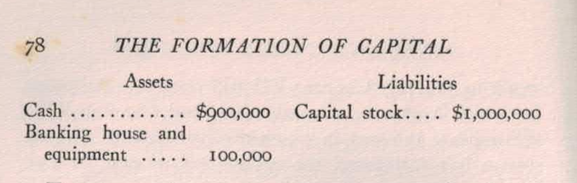

Let us assume, then, that a group of individuals within

an isolated community decides to form a commercial bank with a capital of a

million dollars. Ten thousand shares of stock are issued at $100 per share.

This stock is set down as a liability of the bank, inasmuch as it represents

the obligation of the banking corporation to the shareholders. After an outlay

of $100,000 for a bank building and the necessary furniture and fixtures, the

preliminary financial statement of such a bank would stand as follows:

Two types of operations may be expected to begin almost

immediately. First, certain individuals — stockholders, and others — will

deposit with the bank cash which has hitherto been held in their own strong

boxes. If, in the course of a few months, deposits in the amount of $100,000

are made and there are no withdrawals, the balance sheet will show, in addition

to the foregoing items, new assets in the form of cash of $100,000, and new

liabilities in the form of deposits (owing to depositors) of $100,000. Such

deposits would be identical in character with those which individuals would

make at a savings bank.

It is the second type of operation, however, which

constitutes the essential characteristic of the commercial bank. The bank, when

it opens its doors, states not only that it solicits deposits of cash but that

it is in a position to make loans to merchants, manufacturers, and others.

These loans, as we shall see, result in new deposits against which checks may

be drawn in the same way as they are drawn against deposits of actual cash.

It is how the

commercial bank creates money that we will start to look at next Tuesday.

#30#